The oil market is at a critical juncture, with the dynamics of supply and demand presenting a puzzle that seems difficult to solve. While crude oil prices are struggling to stay above $70, the global energy landscape is shifting in a way that may impact the availability of products such as gasoline and diesel. The reason for this paradox lies in the complex interactions between China’s declining crude imports, its struggling refineries, and the subsequent strain on product inventories worldwide.

China, the world’s No. 3 oil product consumer and producer, has been experiencing a significant decline in crude imports since June. The latest data shows a 4.7 million barrels per day (b/d) year-over-year drop, with teapot refineries operating at only 50% capacity. This is in stark contrast to the US refineries, which are running at a high utilization rate of 95%, and the refineries in PADD 2, which are operating at over 100% capacity.

Despite China’s reduced crude imports, product demand remains strong. However, the country’s production shut-ins, estimated at around 8 million b/d, have resulted in a substantial loss of barrels. While China is not importing crude, it is drawing down its product inventories rapidly, which, unfortunately, has no visibility into how low product levels are. It’s reasonable to assume that these levels are near critically low.

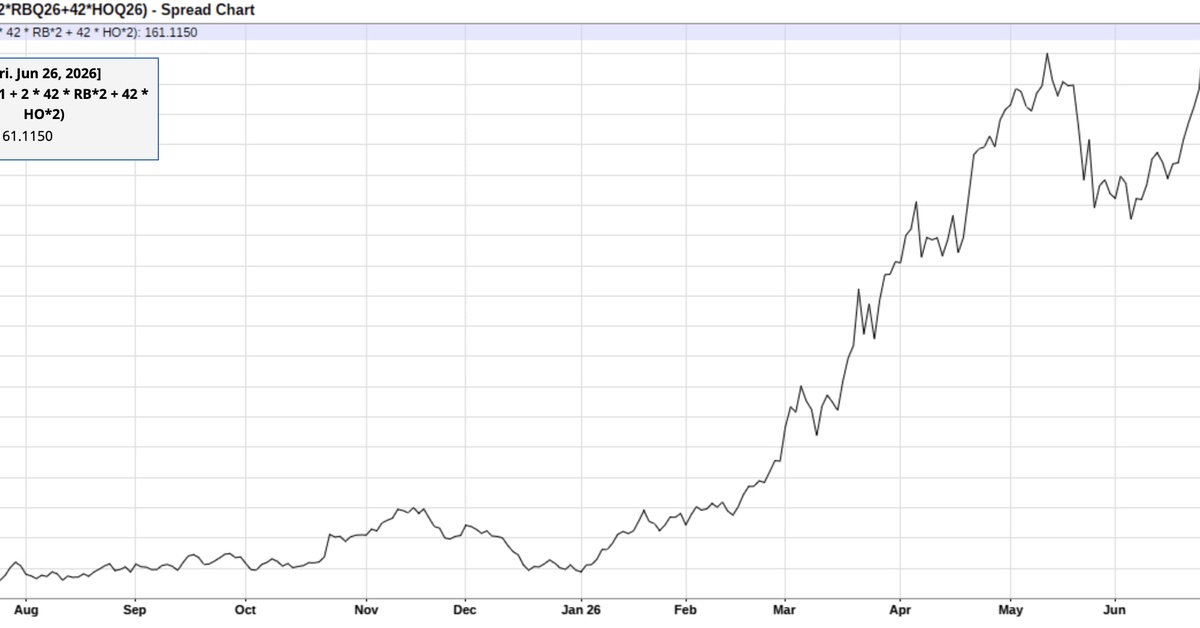

The elevated crack spreads, which represent the price difference between crude oil and its products, are indicative of a shortage of products in the global market. As refineries increase their throughput in the coming weeks and months, the lack of available products will intensify, further pushing these spreads even higher.

The world is bracing for a perfect storm of a global energy imbalance, with the lack of product availability and the resulting higher prices. The ban on product exports from China adds to the complexity of this situation, and it remains to be seen how effectively it will be lifted to address the issue at hand.