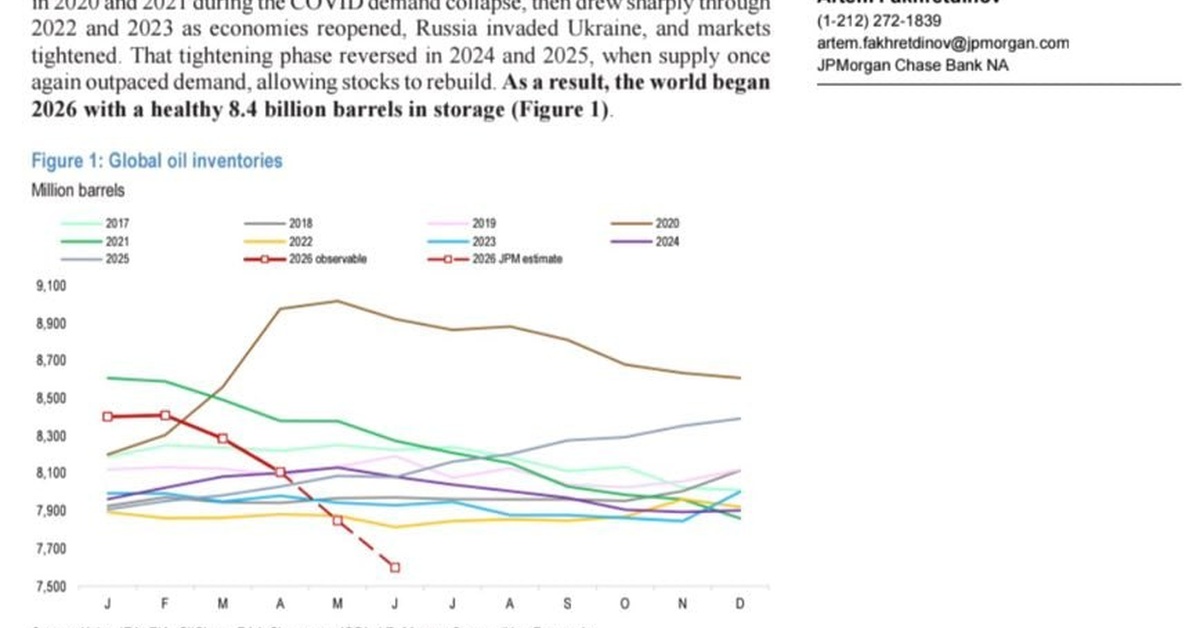

Global oil storage inventories have become a critical balancing mechanism in the current war-driven market shock, according to a JP Morgan flash note. The location and scale of oil supply losses have led to a rapid depletion of inventories rather than an immediate mobilization of spare production capacity. Analysts at JP Morgan suggest that a majority of the global oil storage capacity is comprised of 8.4 billion barrels, with 6.6 billion stored onshore and 1.8 billion stored offshore.

Offshore storage includes a substantial proportion of crude and refined products, such as Russian and Iranian oil, which are effectively functioning as floating storage. However, some of these barrels in transit are simply waiting to be transferred to customers, highlighting the complex nature of global oil storage. Visibility into storage levels varies significantly, with OECD inventories being relatively transparent due to the maintenance of strategic reserves and timely data publication. In contrast, non-OECD countries lack standardized data collection and publication, making storage levels difficult to determine.

China serves as a notable exception, with estimated oil storage levels of around 1.3 billion barrels. JP Morgan’s analysts emphasize the distinction between strategic petroleum reserves and commercial inventories. Commercial inventories are those used in the normal course of trade and refining, whereas strategic reserves are state-controlled emergency stocks.

While storage levels initially appear to provide a comfortable buffer against the oil shock, JP Morgan estimates that a significant proportion of barrels will be inaccessible over the next few months. The accessible portion of onshore storage amounts to around 580 million barrels, leaving the remaining capacity locked up in operational constraints such as pipeline fills and minimum tank levels.

Inventory floors play a crucial role in determining the resilience of oil markets. A market can maintain millions of barrels without any issues as long as working stocks do not fall too low. However, once working volumes decline, the pipeline network loses flexibility, terminals struggle to load efficiently, and refiners face difficulties in securing the necessary oil grades on time. This highlights the critical importance of maintaining a sufficient inventory to ensure smooth oil circulation.

In a prolonged disruption scenario, oil demand can be rationed to maintain inventory levels, resulting in reduced consumption and a broader economic slowdown. A full drawdown of global oil inventories is unlikely, as the sequence of inventory draws tends to prioritize accessibility, economic cost, and logistical ease over the sheer volume of barrels. Oil-on-water and floating commercial stocks are drawn upon first, followed by commercial onshore stocks, strategic petroleum reserves, demand destruction, and operational minimum stocks.

JP Morgan’s analysts predict that OECD commercial stocks could decline to operational minimum levels by September, assuming that the Strait of Hormuz is not reopened and demand destruction stabilizes at 5.5 million barrels per day. The note concludes by emphasizing the intricate dynamics of oil storage levels and the importance of understanding the global oil system’s operational constraints to anticipate and cope with future market disruptions.